This week’s Market Insights opens the third quarter with a real shift in tone across global markets. A much weaker than expected American jobs report has traders rethinking how far the Federal Reserve will push its fight against inflation, while progress in Middle East peace talks keeps draining the fear premium out of energy. Add a yen at generational lows and central banks around the globe pulling in different directions, and the backdrop turns genuinely complex, equal parts risks and opportunity. Below, we analyze gold, oil, currencies, and stocks, and where the cleanest trades hide.

Quick Summary Box

The week opens cautiously risk-on, but everything bends around Wednesday’s Fed minutes. Gold arrives with momentum after soft US employment data cooled rate-hike predictions; buyers need the metal to hold its floor while it grinds through overhead resistance. WTI leans lower, Washington–Tehran diplomacy is advancing, Strait of Hormuz tanker traffic is recovering, and extra supply weighs, though one bad headline flips the script fast. The S&P 500 rides its early-July seasonal tailwind on the innovation trade, healthy corporate revenues, and improving confidence into earnings season. The dollar index has stalled after a strong run, firm, but less sure the Fed hikes at all this year.

Asset Breakdown: Market Research on Global Markets

Our comprehensive methodology is easy to describe and hard to shortcut: gather timely prices, pull the latest insights and forecasts from leading bank research desks, the same work that helps guide businesses, investors, and analysts across geographies, then convert a deep understanding of each driver into actionable intelligence. That’s the heart of these Market Insights.

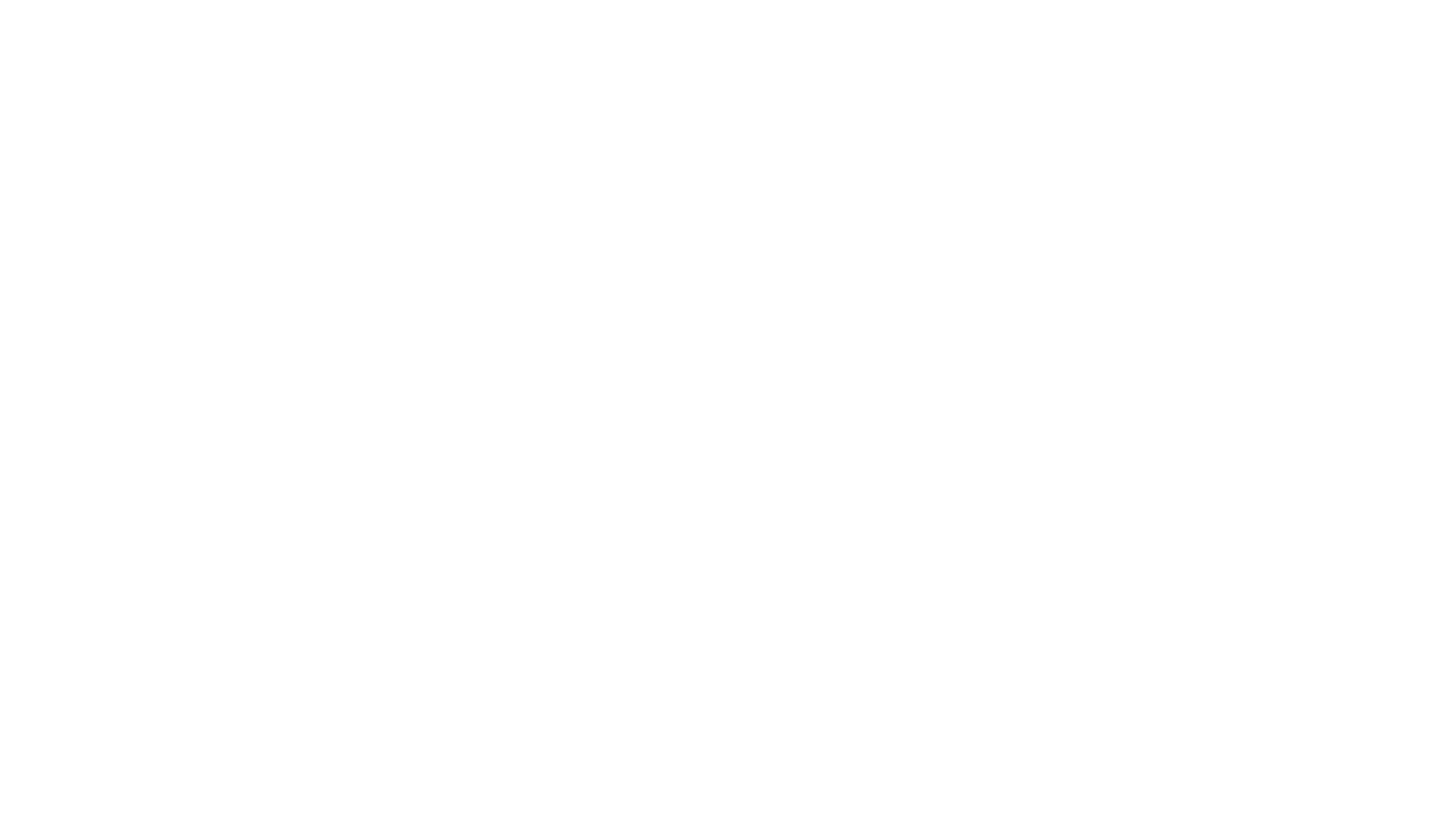

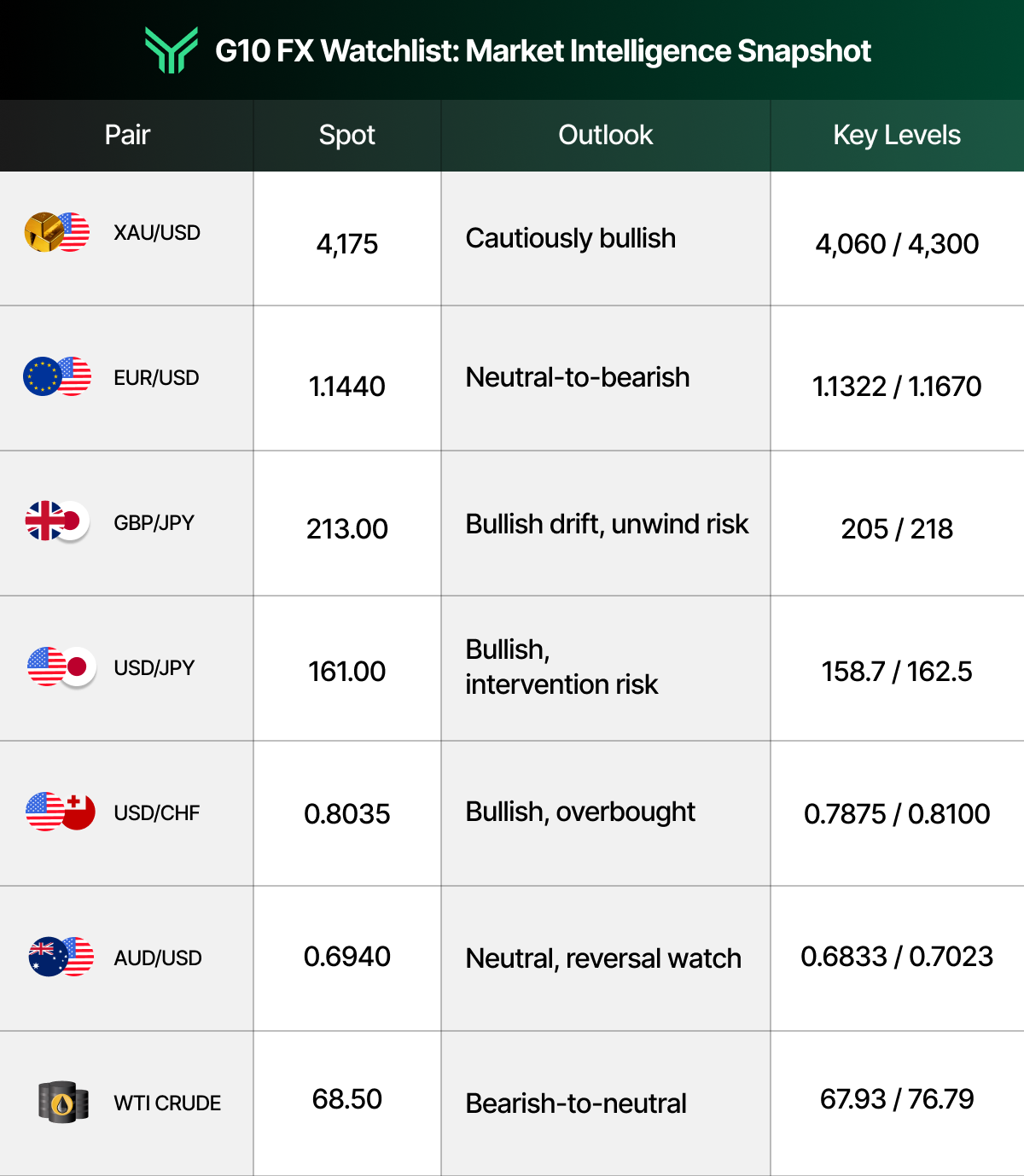

XAUUSD (Gold)

Gold closed the holiday week near $4,175 per ounce, up about 2%, its first weekly gain after four losing weeks. June payrolls added just 57,000 jobs versus roughly 110,000 expected, and September Fed-hike odds fell from 66% to near 50% on CME FedWatch. Cheaper-money bets lifted the non-yielding metal from a weekly low near $3,942 back above $4,170 as safe-haven demand stayed firm.

Zoom out and this is still a correction inside a bull market, the record near $5,595 hit in late January before a drop of more than 25%. Banks have trimmed targets: Goldman Sachs cut its end-2026 call to $4,900 from $5,400 in June, and J.P. Morgan recently lowered its projection to around $5,000 for the fourth quarter. Central banks keep buying, a net 41 tonnes in May per World Gold Council data, supporting a structural floor.

For the week, $4,150 is first support, then $4,060–$4,070, with $3,960 the make-or-break level; resistance: $4,200, then $4,250–$4,300. Monday’s ISM services PMI and Wednesday’s minutes, which may reveal how divided the committee is, are the catalysts; recent commentary from Chair Kevin Warsh already hints the urgency to hike has faded.

Setups like gold’s defend-the-floor rebound are what funded capital exists for. To celebrate freedom and independence, FundingTraders upgraded its biggest offer ever: 55% off, a 100% lifetime Profit Split, and a 250% Refund Bonus, 2.5x your fee back as a bonus with your first payout. All account types, unlimited uses, limited time. Use code 250.

EUR/USD

The euro trades near 1.1440 after a bruising June dragged it from a January high above 1.2016 to a low around 1.1322, the weakest since May 2025. The twist: both central banks are hawkish. The ECB raised its deposit rate to 2.25% in June, and markets project near-even odds of another hike in September, while the Fed dropped its easing language entirely. Aggregated forecast paths banks publish for clients, compiled by Exchange Rates UK, still point to roughly 1.1632 by September and 1.1756 by December, framing current prices as cheap.

Supports that matter: 1.1380 and the 1.1322 low; sellers sit at 1.1516–1.1535 with the 200-day average near 1.1670 overhead. Eurozone retail sales Monday and Germany’s final CPI Friday fill in the economic picture; the minutes pick the direction.

GBP/JPY

Sterling buys about ¥213, near the top of this year’s ¥205–218 range and roughly 36% above the ten-year norm near ¥157. The Bank of Japan lifted its policy rate to 1.00% in June, the highest since 1995, yet the yen keeps sagging: the rate gap still pays carry traders to stay long.

The weaknesses are structural: when global risk spikes, carry positions unwind violently, the August 2024 episode is the textbook example, a collapse from ¥208 to ¥183 in three weeks. With Tokyo weighing intervention and the BoJ meeting July 30–31, treat ¥208 and ¥205 as the levels protecting the uptrend, ¥216–218 as the cap, and keep size honest.

USD/JPY

The yen is the weakest it has been against the dollar since 1986, with USD/JPY hovering around 161.6 The yen touched 162.5 per dollar last week, its weakest in four decades, then snapped back below 161 after a Reuters report said Japan may stop signaling intervention in advance and start targeting speculators instead, just as soft US jobs data hit the dollar. Finance Minister Satsuki Katayama repeats that authorities can act at any time, and thin summer volume makes surprise action more effective.

The carry math still favors the dollar, the Fed at 3.50%–3.75% versus the BoJ’s 1.00%, and futures still lean toward one US hike by year-end. Institutional perspectives on year-end fair value are unusually spread: published 2026 calls run from about 150 (Scotiabank) and 153 (ING) to 164 (J.P. Morgan). Near term, 162.5 is the ceiling; support layers near 160.0 and 158.7. Chasing longs into intervention territory is how accounts get hurt.

USD/CHF and AUD/USD

USD/CHF, near 0.8035, is testing major resistance at 0.8100 in overbought conditions. The Swiss franc remains the world’s classic defensive currency, so geopolitical flare-ups knock this pair lower fast; first support 0.7960, then 0.7875.

AUD/USD, near 0.6940, is down about 4.5% from its monthly highs and leaning on multi-month trendline support, where an outside-day reversal hints the selling is fading. Australia’s cash rate sits at 4.10% after a quarter-point RBA hike, and two events matter doubly for the Aussie: Thursday’s China CPI, Chinese customers take the bulk of Australia’s commodity exports, and Wednesday’s RBNZ decision, where markets price an 80% chance of a hike to 2.50%. Resistance: 0.6943, then 0.7003–0.7023; support: 0.6880, 0.6861, and the key 0.6833.

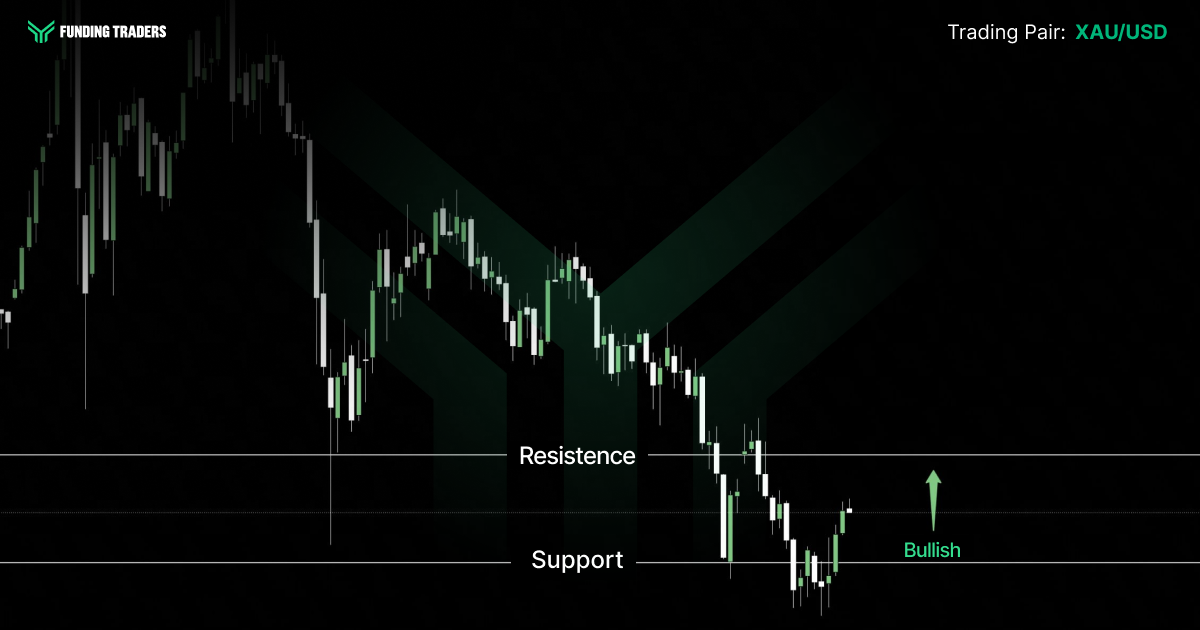

WTI Crude Oil

WTI starts the week near $68.50 after slipping about 2.5%, and the story has flipped from fear to surplus. Indirect US–Iran talks in Doha are progressing, Strait of Hormuz shipping keeps recovering after two vessels were damaged in late June, and easing sanctions on Iran add barrels to a market where US production runs at record highs. Asian demand has returned slower than the industry hoped; Brent has drifted into the low $70s, essentially pre-conflict territory.

LiteFinance’s July forecast range runs $51.99–$76.79, with this week’s band near $67.93–$71.84. Midweek API and EIA inventories plus any Doha headline are the catalysts. The process: sell strength while diplomacy holds, and respect the tail risk, one bad night in the Gulf re-prices everything for traders and oil-importing businesses.

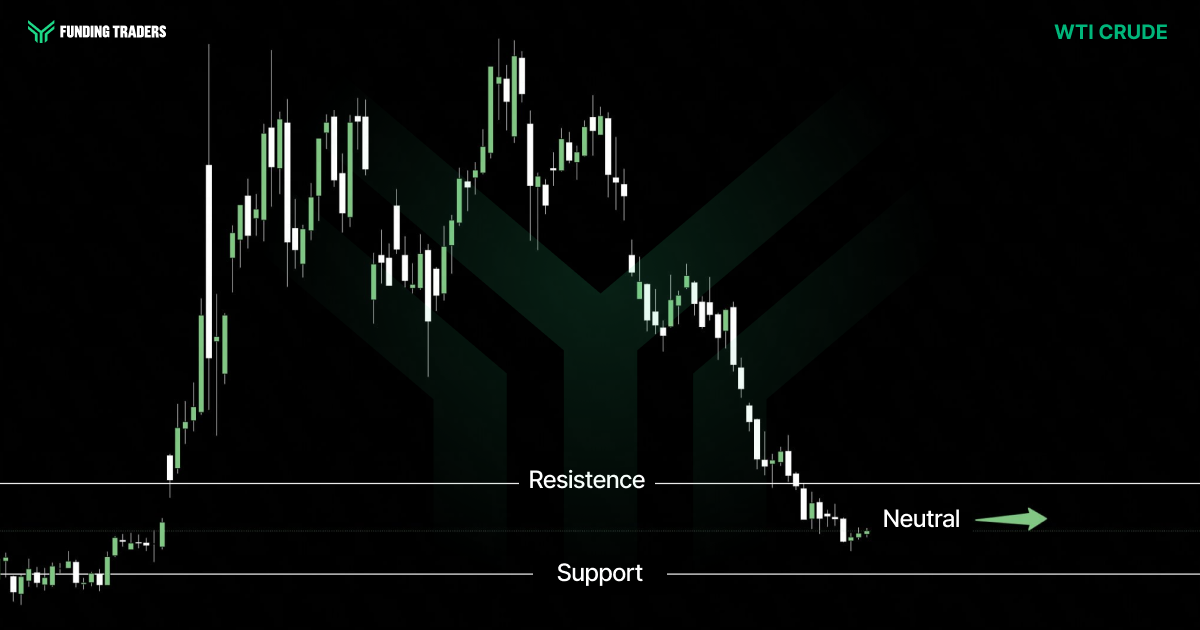

Key Economic Events: July 6 – July 10 (GMT+3)

This condensed calendar is adapted from the Forex Factory economic calendar at forexfactory.com, a leading resource professional traders use to track market‑moving macro news and central bank events in real time.

Asset Watchlist: Market Intelligence Snapshot

All levels are drawn from current technical research and are reference points, not guarantees.

Actionable Insights for the Week to Drive Growth

Preparation is the trader’s edge, the depth of your prep, not the boldness of your ideas, decides the week. A new quarter starts now, so treat these Market Insights as a quarterly market update as much as a weekly plan, and let the calendar inform your sizing. Solo or inside a larger organization, the quality of execution beats quantity, no training course replaces a written plan.

The base case. While diplomacy holds and the Fed stays paused: buy gold pullbacks that hold above $4,150, targeting $4,200 then $4,300, invalidated below $4,060. Sell WTI strength into $71.50–$71.84, targeting $68.00, with a hard stop-loss above $72.50. Fade EUR/USD rallies into 1.1516–1.1535 unless the minutes read dovish. In equities, buying S&P 500 dips toward the 7,400–7,460 gap fits July seasonality. Implement each idea with sizing, stop-loss, and invalidation written before entry, on sensible leverage, the discipline that passes a prop firm challenge and keeps drawdown on a funded account under control.

The triggers. Hawkish minutes revive the dollar and press gold toward $4,060, possibly $3,960, flip short below $4,150 only with confirmation. A Doha breakdown or fresh Hormuz incident sends WTI back through $72.00 and bids gold, the franc, and the yen. An RBNZ hold against 80% hike pricing knocks the kiwi and drags the Aussie. If Tokyo moves from words to actual intervention, yen crosses can drop hundreds of pips in hours, cut GBP/JPY and USD/JPY longs first, ask questions later. Keep CME FedWatch and a live calendar open: access to information is cheap; the edge is acting on knowledge with patience, letting the market come to you and making the data deliver.

If your Phase One plan triggers, trade it with real capital behind you.FundingTraders’ Independence offer is live: 55% off any evaluation, a 100% lifetime Profit Split, and a 250% Refund Bonus paying 2.5x your fee back with your first payout, every account type, unlimited uses, while it lasts. Enter code 250.

Stay Ahead of the Market

The framework is clear: a soft jobs report loosened the Fed’s grip without breaking it, oil’s fear premium keeps deflating, gold is trying to turn a bounce into a bottom, and the yen is stretched enough that one Tokyo headline could shake every cross. Wednesday’s minutes tie it together, confirming the pause or showing a committee still itching to hike. Explore each level on your own charts before the open.

That’s the purpose of these Market Insights: a comprehensive view of the week, distilled into action. FundingTraders is a proprietary trading firm built for these conditions, a brand trusted by funded traders worldwide, with unrestricted news trading, weekly payouts, a transparent scaling plan, an industry-leading profit split, and trading rules with risk limits that reward consistency. A clear payout process and the firm’s dedicated support team stand behind every evaluation, across all account types and major platforms, so getting funded matches how you actually trade. Our funding programs and community exist to put trading capital behind traders with a plan, built by traders, for serious traders.

Prepare the levels, respect the triggers, and stay patient, the traders who profit most this week will be the ones who planned it in advance and had the capital to express high-conviction macro setups when they appeared.

This is the week, and the offer, to go bigger. In celebration of freedom and independence, FundingTraders upgraded its biggest deal ever: 55% off, a 100% lifetime Profit Split, and a 250% Refund Bonus, 2.5x your fee back as a bonus on your first payout. All account types. Unlimited uses. Limited time only. Claim it with code 250.

Disclaimer: Trading involves significant risk and is not suitable for every investor. Past performance is not indicative of future results. The information provided in this article is for educational and informational purposes only and should not be considered financial, investment, or trading advice. All account rules, payout structures, profit splits, and promotional offers described in this article are subject to change at the discretion of FundingTraders. Promo codes may expire or be modified without prior notice. Always trade responsibly and only risk what you can afford to lose.